The aviation industry across the globe, and particularly in India, is experiencing a period of unprecedented growth. Supported by favorable government initiatives, advancements in technology, and rising disposable incomes, the surge of new airlines and aviation-related companies is remarkable. However, as history teaches us, such booms are often followed by corrections, leading to a potential consolidation phase through mergers and acquisitions (M&A). This article will explore the current dynamics of the aviation sector, provide detailed statistics, case studies, and a comprehensive outlook on the future of M&A in this industry.

Current Landscape of the Aviation Industry

Statistical Growth Overview

The aviation sector has shown impressive growth rates in India. The following table illustrates the increase in air passenger traffic over recent years, highlighting the sector’s upward trajectory:

| Year | Domestic Passengers (Millions) | International Passengers (Millions) | Growth Rate (Domestic) | Growth Rate (International) |

|---|---|---|---|---|

| 2018-2019 | 341.04 | 69.74 | – | – |

| 2019-2020 | 348.63 | 77.25 | 2.12% | 10.73% |

| 2020-2021 | 140.80 | 16.81 | -59.73% | -78.24% (Pandemic Effect) |

| 2021-2022 | 165.20 | 28.76 | 17.44% | 71.42% |

| 2022-2023 | 220.00 | 40.00 | 33.33% | 39.14% |

Table 1: Air Passenger Traffic Growth in India

Key Growth Drivers:

- Infrastructure Development: Enhanced airport infrastructure, including the construction and modernization of terminals, is facilitating increased passenger flow. Simultaneously, allotment of prime spaces to FTOs, MROs and other ancillary aviation companies next to remote airstrips adding to the boom.

- Digitalization: The adoption of technology in ticketing, customer service, and maintenance operations is making air travel more accessible and efficient. Long gone are the days of Travel Agents taking you for a ride.

- Environmental Regulations: Increasingly stringent emissions regulations are prompting innovations in aircraft technology, which will affect both operational costs and market dynamics.

- Government Support and Initiatives to boost Aviation Industry

The Surge in New Entrants

Industry Entry Analysis

Over the past few years, the Indian aviation market has seen the introduction of numerous players.

As per DGCA present stats in India:

Total Non-Scheduled Operators (NSOPs): 117

Applications pending with DGCA for grant of NSOP: Approx 77

Total Scheduled Airlines: 12

Major players: Indigo and Air India enjoying a duopoly with aircraft numbers to the tune of 300 each

Several Regional Airlines like Air Kerala, Al Hind, Shankh Air etc are jostling to pick up a pie of the Scheduled Airlines space in 2025, though regional to start with.

However, not all of these will be able to sustain their operations, leading to the following trends:

Case Study: The Rise and Challenges faced by Airlines

- Akasa Air: The Mumbai-based low-cost airline, which started operations about three years ago, has a fleet of 27 planes, but has 226 jets – all Boeing 737 MAXs – on order. Deliveries have been delayed as Boeing’s 737 program faced regulatory scrutiny after a mid-air cabin panel blowout last year and suffered from the effects of a seven-week workers’ strike. Troubles at Akasa with large unutilized pilots and engineers is having a ripple effect on their planned expansion.

- Spicejet: Though pulling on for a long time, Spicejet is presently facing fresh round of troubles as three Ireland-based aircraft lessors, viz NGF Alpha, NGF Genesis and NGF Charlie- have filed petitions in NCLT under Section 9 of IBC, seeking initiation of insolvency proceedings against SpiceJet claiming dues totalling USD 12.68 million (about Rs 108 crore).

- GoAir (Go First): Launched in 2005, GoAir has faced funding challenges and operational hurdles but managed to manoeuvre for a sufficiently long time by focusing on low-cost travel options. However, the company finally had to shut shop after a Court Order deregistered all it’s aircraft, highlighting the challenges airlines face in a competitive marketplace.

- IndiGo: As a successful low-cost carrier, IndiGo has managed to grow its market share significantly, outperforming many competitors through operational efficiencies. It serves as a benchmark for emerging airlines aiming to sustain themselves long-term.

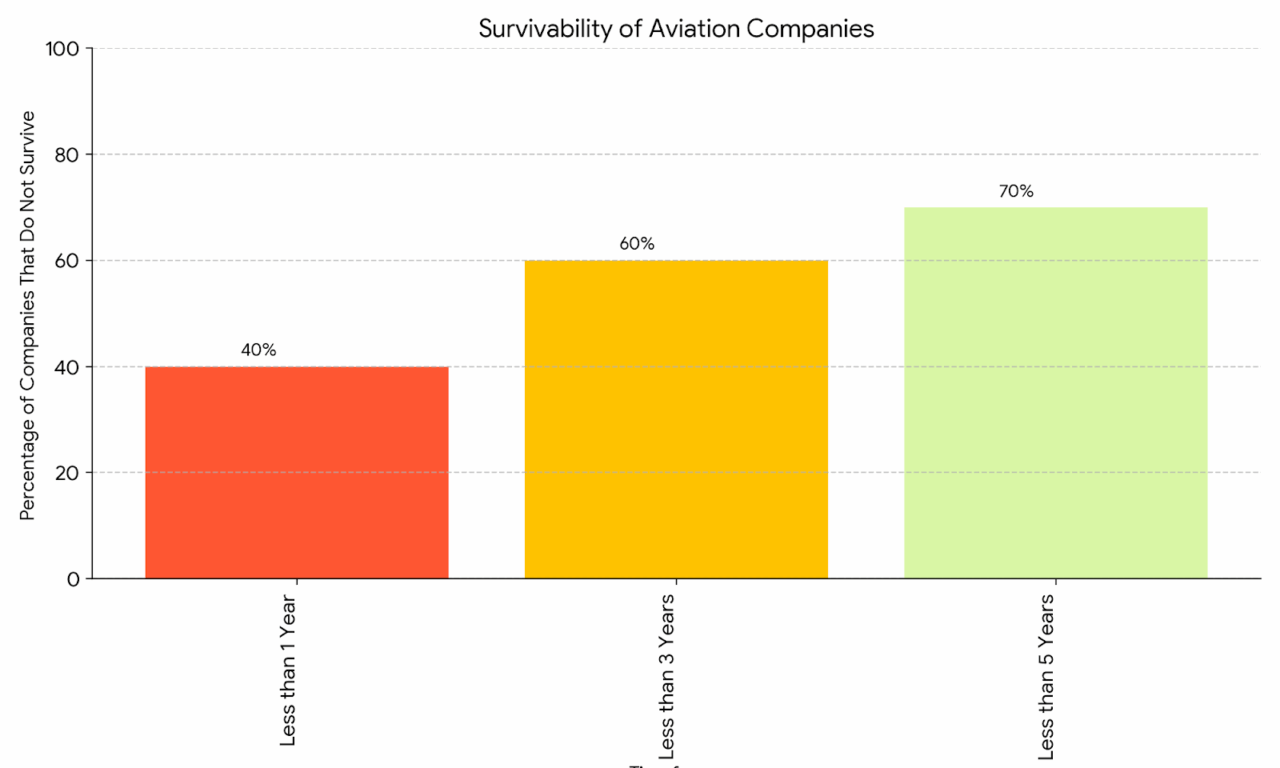

Survival Rates of New Airlines

The probability of survival for new airlines is illustrated in the chart below, showcasing a typical trend in the aviation sector:

- Less than 1 Year: 40% of new entrants do not survive.

- Less than 3 Years: 60% do not make it past this point.

- Less than 5 Years: Only 30% endure.

Chart 1: Survival Probability of New Airlines over 5 years thus drops to 30%

This trend raises significant concerns about market saturation and the impending consolidation phase.

The Inevitable Trough: Triggers for Consolidation

Indicators Reflecting Impending Consolidation

- Market Overcrowding: The influx of airlines may lead to a lack of differentiation, increasing competition. Many new entrants may struggle to maintain profitability, increasing the likelihood of acquisitions.

- Financial Instability: Many newer scheduled and non-scheduled airlines are bound to face challenges in achieving financial sustainability. As cash reserves dwindle and operating costs rise, they will become vulnerable to acquisition while the smarter ones amongst them will opt for mergers or opt for inducting managing partners who with their professional skills could possibly achieve turnarounds.

- Owners lack of business acumen: As is the culture and herd mentality, many HNI’s get attracted to the glitz and glam of the aviation industry, thereby investing colossal sums into it while trivializing the challenges inherent to aviation. Lacking the right business acumen topped with unprofessional management, eventually lead to such companies shutting shop, leaving the flamboyant owners to face the flak.

- Regulatory Environment: Manoeuvring through and complying with the stringent regulatory norms characteristic to any Aviation Industry is not for the weak hearted. Regulatory bodies will eventually force consolidation to maintain safety standards and improve operational efficiency among carriers.

Historical Precedence in Aviation M&A

The aviation industry has experienced numerous M&A activities, reflecting the boom-bust cycle effectively. Few famous ones for instance:

- Delta Airlines and Northwest Airlines: The merger in 2008 created the world’s largest airline, showcasing how economies of scale can improve service offerings and reduce costs.

- British Airways and Iberia: Merged in 2011 to form International Airlines Group (IAG), this partnership allowed both airlines to leverage their networks while achieving significant cost synergies. By consolidating operations, they could offer competitive fares and enhance service delivery, demonstrating how strategic mergers can lead to enhanced market position.

- Lufthansa and Swiss International Air Lines: In the mid-2000s, Lufthansa acquired Swiss to enhance its European market reach and operational capacity. This merger aimed at strengthening their competitive advantage against low-cost carriers and other full-service airlines. The integration process, albeit challenging, allowed Swiss to retain its brand identity while benefiting from Lufthansa’s operational expertise.

- Vistara and Air Asia India: In early 2020, Vistara (a joint venture between Tata Sons and Singapore Airlines) acquired AirAsia’s stake in their joint venture, AirAsia India, increasing Vistara’s market presence. This strategic acquisition demonstrated the consolidation trends within the industry.

- Air India and Indian Airlines: In 2007, state-owned Air India merged with Indian Airlines, creating a single entity under the Air India brand. This move aimed to mitigate competition, streamline operations, and enhance service delivery across both domestic and international markets.

- The list is endless with mentions of Jet Airways taking over Air Sahara (2006), Kingfisher and Deccan Airlines (2007), Spice Jet and Kalanithi Maran’s group (2010), Jet Airways and Etihad Airways (2013) etc etc.

Similar is the list of Airlines going bust with some leading names being Jet Airways, Kingfisher Airlines, Paramount Airways, Go Air (Go First), Indus Airlines etc etc.

These historical examples underscore the cyclical nature of the aviation industry, with periods of rapid growth often followed by consolidation as companies seek to stabilize and optimize operations.

Future Landscape: Predicting M&A Trends in Aviation

Implications for Market Players

As the aviation industry evolves, several implications regarding M&A trends can be drawn:

- Increase in Strategic Alliances: Companies will increasingly seek partnerships not just through mergers, but also through strategic alliances and joint ventures, allowing them to share resources, reduce costs, and enter new markets without the need for full mergers. Many companies, mostly from the General Aviation sector, with full knowledge of the DGCA, have already resorted to sharing their manpower through cross utilization contracts, to tide over the shortages like for example the B2 Engineers that are rare to find.

- Focus on Sustainability: Companies demonstrating commitment to sustainability and environmental responsibility will likely be more attractive acquisition targets, especially as regulations become stricter and consumer preferences shift toward eco-friendliness.

- Technology as a Catalyst: The role of technology will be crucial in the M&A space, as companies that leverage innovation effectively will outpace competitors. Acquiring tech-driven startups focused on areas such as AI in customer service, automation in logistics, and data analytics can provide competitive advantages.

- Globalization of Operations: Emerging players can orient their strategies toward global markets, identifying acquisition targets in different geographies to diversify their portfolios and expand their reach.

Challenges for New Entrants

New entrants must navigate several challenges as they step into this competitive landscape, which could push many toward M&A:

- Securing Funding: Access to capital remains one of the most significant challenges, especially following the economic impacts of the COVID-19 pandemic. New airlines may rely heavily on investor funding and venture capital, often transforming their business strategy to align with investor expectations.

- Navigating Regulatory Hurdles: Regulatory requirements can pose significant barriers to entry and ongoing operations. New companies must demonstrate compliance and risk management capabilities to survive, which can be taxing on resources.

- Overcoming Lack of Business Skills: Promoters and Owners will have to go the extra mile in identifying the right management to be placed at the helm of such organizations. While Integrity remains non-negotiable, professional and proactive approach of the management in an aviation company could swing the EBITDA by as much as +/- 30%. Some Owners of late have started offering stakes to indispensable CEO’s and MD’s, somewhat similar to ESOPs practiced by MNC’s.

- Consumer Behavior: Changing consumer preferences, especially after the pandemic, will require agility in service offerings. Airlines’ ability to adapt to the evolving expectations of travelers—such as enhanced hygiene practices and flexible booking policies—will be critical for survival.

Late-Stage Entrants: Strategic Advantages in Acquisitions

Late-stage entrants can also find unique opportunities amidst the turbulence. By observing industry trends and learning from the mistakes of early entrants, they can position themselves strategically:

- Targeting Failures: Late entrants can analyze and identify struggling airlines / aviation companies and strategically acquire them at lower valuations. These acquisitions can help build market share quickly and allow the integration of established customer bases.

- Geographical and Service Diversification: By strategically expanding service areas or targeting underserved markets, late entrants can find niches that allow them to capture market share while existing competitors grapple with their challenges.

- Emphasizing Value Propositions: New players entering the market should prioritize strong value propositions, leveraging technology, customer service, and unique offerings to differentiate themselves from established competitors.

Case Study: An Emerging Airline’s Journey

To illustrate the challenges and opportunities for emerging airlines, let’s consider the hypothetical example of “AeroStar”, a new entrant launched in 2023 and its modus operandi:

- Foundational Approach: AeroStar focused on niche markets in Tier 2 and Tier 3 cities, tapping into unmet demand for regional travel. Its business model was designed around affordability and convenience, targeting price-sensitive travelers.

- Technology-Driven Operations: Leveraging digital platforms and AI for ticketing and customer engagement, AeroStar aimed to achieve operational efficiencies through automation and advanced analytics. By utilizing customer data to tailor services, AeroStar positioned itself favorably among tech-savvy consumers.

- Professional Management: Aerostar left no stones unturned to attract the best talent in the aviation industry, thereby appointing and placing an efficient management at the helm.

- Funding Strategies: To navigate capital challenges, AeroStar sought partnerships with venture capital firms specializing in transportation. These strategic funds allowed for aggressive marketing and service launch while setting the groundwork for potential acquisition.

- Future Outlook: As AeroStar continues to grow its fleet and customer base, being agile in partnerships and remaining responsive to market demands will be crucial. Achieving visibility and goodwill in the aviation marketplace positions it as a potential consolidation target for established players looking to venture into new regions.

The Role of Government Policies and External Factors

Governmental Support as a Catalyst

The role of government policy in bolstering the aviation industry cannot be overstated. Policy initiatives can stimulate growth and influence M&A. Government policies can significantly influence the aviation landscape. In India, the government’s strategic initiatives, such as the National Civil Aviation Policy (NCAP) and supportive measures through the Ministry of Civil Aviation, aim to foster growth and investment in the sector. Some specific initiatives are:

- Udaan Scheme: Launched to enhance regional connectivity, this scheme has encouraged airlines to operate in underserved airport markets and incentivized them through financial support. The expansion of domestic routes has provided fledgling airlines with new opportunities for growth.

- FDI Policy: The government’s Foreign Direct Investment (FDI) policy allows for 100% FDI in air transport services and opens the door for foreign airlines to invest in Indian carriers. This influx of foreign capital can provide established airlines with the funds necessary for expansion.

- GST Reduction from 18 to 5%: The GST on domestic MRO services has been reduced from 18% to 5%. A uniform 5% IGST is now applied to all aircraft and aircraft engine parts, regardless of their HSN code. Helicopter services are subject to a 5% GST w.e.f. Oct 10 2024. This policy change addresses challenges like inverted duty structures, GST accumulation, and customs classification ambiguities, making India a more attractive destination for MRO services.

- Privatization of Airports: The trend towards privatization of several major Indian airports allows businesses to operate with improved efficiency and customer service standards, creating a competitive atmosphere that supports both growth and consolidation. The Government’s policy of allotment of land next to remote airstrips has also paid off well as can be seen in the case of Jalgaon (Maharashtra) and Khajuraho (Madhya Pradesh) where FTO’s like FlyOla, Skynex, Shaurya Flight Sim etc are flying high with hefty bottomlines.

- Regulatory Framework: Regulatory bodies such as the Directorate General of Civil Aviation (DGCA) influence the operational landscape of airlines. New entrants must navigate rigorous compliance processes that are characteristic of Aviation Industry across the world. This often significantly affects their sustainability and thus raises potential for mergers.

External Factors Influencing the Aviation Market

- Economic Conditions: The health of the global and national economy is a crucial factor. Economic growth often boosts disposable income and consumer travel demand. Conversely, economic downturns may lead to reduced travel budgets, affecting airline revenues.

- Global Events: Events such as the COVID-19 pandemic dramatically alter the trajectory of the aviation industry. The pandemic forced a reckoning in how airlines operate, highlighting the need for resilience and adaptability. Future disruptions—be they health crises or geopolitical tensions—will also dictate operational tactics.

For example the recent tariff war started by President Trump, even though predicted to be short term, with China retaliating and asking it’s Airlines not to take deliveries of Boeing aircraft (instead accelerating it’s COMAC C919 and C929 aircraft) could in one way be damning for Boeing. But at the same time these white tail aircraft (aircraft manufactured on order but not picked up) could be a boon for Airlines in India reeling under extremely delayed deliveries. To gauge the extent, Air India and new entrant Akasa Air have ordered 446 Boeing jets in total since 2021, roughly half of the aerospace company’s total orders from Central, East, South and Southeast Asia. Boeing is yet to fulfill delivery of 178 planes to Air India and 199 more to Akasa, according to the company - Technological Advancements: As technology evolves, so too do customer expectations. Airlines must continually innovate, implementing the latest advancements in AI, machine learning, and big data analytics to enhance the passenger experience. Companies leveraging technology effectively can improve operational efficiencies and provide a better service, which may lead them to become more appealing acquisition targets.

- The Sanctions Era: The United States hegemony and the practice of placing sanctions on any country that doesn’t tow it’s line, has proven to be a bad omen to the Aviation Industry of many a countries. The Indian Air Force for example comprises of an inventory that is almost 70% of Russian origin. Placing sanctions on Russia or Iran thus becomes detrimental to the interests of developing countries like India that are still struggling to catch the bandwagon of progress by accumulating resources from every possible source. This needs to change.

Conclusion: Preparing for the Future of Aviation

The aviation industry stands at a critical juncture filled with opportunities and challenges. As companies navigate this boom-bust cycle, the likelihood of mergers and acquisitions will increase, reshaping the landscape significantly.

The key to success lies in understanding market dynamics, leveraging government support, maintaining financial viability, and focusing on sustainable practices. Emerging players should remain agile and learn from established carriers’ journeys, ensuring they create robust business models to navigate the complexities ahead.

Strategic Recommendations for Various Stakeholders

For New Entrants:

- Understand Regulatory Requirements: Most Important aspect for an NSOP to survive, So:

– Stay Compliant: Familiarize yourself with the regulatory landscape governed by the Directorate General of Civil Aviation (DGCA) in India. Ensure compliance with licensing, safety regulations, and operational guidelines.

– Obtain Necessary Licenses: Secure all necessary permits and licenses before commencing operations. This might include Air Operational Clearance (AOC) and adherence to safety and operational standards.. - Build Strong Brand Identity: Cultivate a clear brand message that resonates with target customers. Differentiation is key; airlines must create unique selling propositions that distinguish them from the competition.

- Flexibility and Adaptability: Being nimble in adapting to market changes can determine longevity. Late-stage entrants can take lessons from early players’ mistakes and adopt best practices that align with consumer preferences.

- Implement Strong AI backed Marketing Strategies: Marketing makes or breaks companies, so should at the forefront through:

– Targeted Marketing Campaigns: Use targeted marketing and advertising strategies to build brand awareness and attract customers. Leverage digital marketing, social media, and influencer partnerships.

– Promotional Offers: Implement introductory fares and loyalty programs to entice travelers and build a loyal customer base in the early stages of operation.

For Established Carriers:

- Explore Diversification: Look for opportunities to diversify services and geographic coverage by acquiring regional operators or ancillary service providers. This can help mitigate risks associated with market fluctuations.

- Focus on Customer Experience: Invest in technology that enhances customer engagement and loyalty. Improved service quality can lead to a stronger position during future M&A discussions.

- Engage in Preemptive Acquisitions: Established airlines should actively identify and engage with potential acquisition targets to consolidate their market presence and avoid reactive strategies in a booming market.

- Invest in Employee Development:

–Training and Development Programs: Invest in comprehensive training programs for employees to enhance skills and improve service quality. Focus on leadership development, customer service training, and ongoing education in aviation operations.

–Employee Engagement Initiatives: Foster a positive work culture through employee engagement programs, recognizing contributions, and promoting well-being. Happy employees are more likely to provide superior customer service.. - Marketing Campaigns: Utilize targeted AI marketing campaigns to reach specific customer segments, utilizing social media, digital platforms, and influencer outreach to enhance visibility and brand loyalty.

For Investors:

- Monitor Regulatory Changes & Govt Policies: Stay updated on government policies that impact the aviation sector. Understanding regulatory landscapes will help in identifying viable investment opportunities. Never forget that In 1953, the Indian government nationalized Air India and several other airlines, including those owned by Tata, effectively ending the Tata’s direct control over these airlines. Decades later, a change in government policy, specifically a privatization drive, led to the Tata Group acquiring Air India in 2022, bringing the airline back under their ownership

- Evaluate Technological Investments: Look for airlines investing in technology-driven solutions that create operational efficiencies or enhance customer experiences, as these companies may yield better long-term returns.

- Risk Assessment & Due Diligence: Assess the financial health, operational efficiency, and sustainability measures of emerging airlines and aviation companies to forecast long-term viability before deciding to go in for investments. Investors should understand that in Airlines business, unlike any other, offloading equity is not easy. Aircraft and Inventory appraisals often have high variance, thereby affecting valuations of companies by huge margins. Due diligence and caution is thus imperative.

- Strategic Diversification: Consider diversifying investments by not only focusing on airlines but also including ancillary aviation services which have an equally huge potential such as ground handling, maintenance, and logistics companies.

- Engage with Experienced Aviation-focused Funds: Seek investment opportunities through mutual funds or private equity firms specializing in aviation. These funds bring industry expertise and diversified exposure to a range of companies.

- Consult Industry Analysts: Engage with analysts who specialize in the aviation sector for insights and forecasts on potential investment opportunities.

- Stay informed about Global Aviation Dynamics: Keep an eye on global aviation trends that may impact the Indian market, such as international travel regulations, fuel price fluctuations, and advancements in aviation technology.

- Benchmark Against Global Peers: Compare airlines in India with international counterparts to evaluate performance and growth trajectories and this helps in making right choices.

Forward-Looking Perspective

The future of the aviation industry holds immense potential, driven by emerging trends in passenger traffic, technological advancements, and governmental support. While challenges will undoubtedly arise, the players best prepared to capitalize on the cycles of boom and bust will emerge as leaders in the highly competitive sector.

As we move forward, the aviation industry must remain vigilant, proactive, and adaptable. By understanding historical patterns and preparing for fluctuations in demand and market dynamics, stakeholders can position themselves effectively to ensure long-term success in an ever-evolving landscape.

{kind=link}